Hi all,

I am moving this blog to investingsight.blogspot.com. This will be my new personal blog for anything investment. Currently, work is still in progress so there will be nothing (at the moment) in that blog. In the meantime, go here to read some articles that I've posted on investment site Seeking Alpha over the past few years. Thanks very much!

Happy Investing!

Kang Wei

Thursday, 15 October 2015

Thursday, 18 December 2014

IBM: An Attractive Long-Term Buy Despite Current Troubles

International Business Machines Corp. (IBM) needs no introduction. It is one of the giants in the technology industry, with nearly $100B in revenue over the last fiscal year. Although this is the case, it has had its fair share of troubles, with stock prices down 18% year-to-date and continually 52-week lows. In this article, I will address some reasons why the Big Blue remains a good deal for investors despite its many troubles. Here is some background information and a snapshot of the company's finances:

Background Information

IBM, founded in 1910 and headquartered in New York, provides IT products and services worldwide. The company's Global Technology Services segment provides IT infrastructure and business process services, including outsourcing, processing, integrated technology, cloud, and tech support. Its Global Business Services segment offers consulting solutions for application innovation and management, enterprise applications and smarter analytics.

The Software segment offers middleware and operating systems software, such as WebSphere software to integrate and manage business processes, information management software, Tivoli software for cloud and data center management, Rational software that supports software development and Mobile Software for platform and application development and mobile.

The Systems and Technology segment provides computing power and storage solutions and capabilities, while its Global Financing segment provides lease and loan financing to end users, including commercial financing to dealers and re-marketers of IT products; and re-manufacturing and re-marketing services for equipment.

Snapshot

| Price (17.12.2014) | $151.93 |

| Market Cap | $150.36B |

| TTM Income | $16.42B (P/E: 9.54) |

| TTM Sales | $96.38B (P/S: 1.56) |

| Book Value per Share | $14.37 (P/B: 10.57) |

| Debt/Equity Ratio | 3.21 |

| Sales Growth Past 5 Years | -0.80% |

| EPS Growth Past 5 Years | 10.90% |

| Current Ratio | 1.10 |

| Dividend | $4.40 (2.90%) |

- Watson is able to read and understand natural language, allowing the system to analyze the unstructured data that makes up almost 80% of data today.

- This opens up a new world of possibilities, allowing data of numerous different forms to be processed and analyzed, including data that could not be analyzed in the past. Such an ability will definitely be valuable to many businesses, giving them deeper insight into their customers and their needs.

- Watson is able to generate a hypothesis and to evaluate relevant information and responses.

- It is not just able to process data, it is also able to see trends and generate hypotheses, which is a feat that will be a great help for businesses in many different industries. The usage of Watson can potentially save on costs of hiring (for companies(, and also reduce the margin of error during analysis.

- Watson is able to learn by tracking feedback from its users, and can hence learn from its successes and failures.

- This allows Watson to continually improve, and allow it to take on new, more advanced roles in analyzing data and generating hypotheses.

| Cost Of Equity=2.07%+(0.63*6%) |

| Cost Of Equity=5.85% |

| WACC=5.85%(2279/2279+3972)+2.53%(3972/2279+3972) |

| WACC=3.74% |

| Terminal Value=Terminal Year Cash Flow/(Final WACC- Terminal Growth Rate) |

| Terminal Value=$8.669B/(5.66%-1.45%) |

| Terminal Value=$206.100B |

| Present Value of Terminal value= Terminal value/(Final WACC)^10 |

| Present Value of Terminal value= $206.100B/ (1.0566)^10 |

| Present Value of Terminal value= $135.117B |

IBM's Troubles

-Revenues on Decline, Further Margin Expansion Limited, Targets Missed

Clearly, IBM has many troubles at the moment. Firstly, IBM is in a transition period now, as it tries to move from a predominantly hardware company to one that is mainly involved in software items. For instance, it sold its x86 system to Lenovo earlier this year for $2.1B, and its chip business to GlobalFoundaries more recently for $1.5B

Although the company is retaining more profitable segments of the company, it is immensely difficult for rapidly growing (but smaller) segments to make up for the revenues lost due to the loss of larger, more mature segments that have been sold off. Such divestitures have resulted in considerably lower revenue for the company over the past few years, as attested to by the IBM sales growth rate over the past 5 years of -0.8%.

Additionally, the company is fuelling earnings growth predominantly by cost cutting. If one looks at IBM's income statement, the cost of revenue has declined by 10% (from 56.8B to 51.2B) over the past 3 years. Although there is still space for more cost-cutting through layoffs and divestitures, this potential for costs to be reduced further will decrease over time. This means that IBM will not be able to utilize widening margins as a method for it to increase earnings despite revenue declines. This is also one of the reasons why IBM has abandoned their 2015 roadmap towards an EPS of $20. It is highly likely that a company in a transition phase can meet growth targets.

-Heavy Competition

Besides this, IBM faces heavy competition from other companies in the sector, like HP (HPQ), Cisco (CSCO), Oracle (ORCL) and Microsoft (MSFT). As shown in this Q3 2014 news report, IBM lost more market share to companies like Dell (NASDAQ:DELL) and Cisco, after losing market share both this year and last year to its competitors in this industry, including HP and Cisco. This was due to weakness in both the high-end mainframe and power server segment, and also the low-end x86 segment. In the cloud segment, where the company is growing revenues fast, it also faces competition from the likes of Microsoft Azure and the Amazon AWS.

Although IBM is a large company with liquidity and R&D capabilities, many of its competitors also have such a quality (some even with better financial positions), which is one of the reasons why it is struggling to grow the revenues in many of its operating segments currently.

-Acquisition & Goodwill Risk

Furthermore, the company has been actively acquiring companies, which poses risks such as an integration risk. This is since the newly-acquired company may not be able to fully integrate into IBM, due to differences in culture and tradition. This will result in lower efficiency, and in some cases, a loss of valuable human capital.

Due to such acquisitions, IBM has also accumulated quite a lot of goodwill, which is not healthy for a company's balance sheet. Goodwill is an intangible asset that arises when a company buys another company, and pays more than the net equity of the company. The difference between the purchase price and the equity is called goodwill. Currently, IBM owns 27.7% of its assets in goodwill and other intangible assets. This has led to a less healthy balance sheet, with shareholders' equity fuelled mainly by goodwill. A recent Seeking Alpha article (here) covers the issue about IBM's goodwill problem in more depth.

IBM's Buy Thesis

As covered above, IBM has many troubles at the moment, but as shown below, investors can still stand to benefit from IBM shares with an attractive buy thesis.

-Shareholder Remuneration

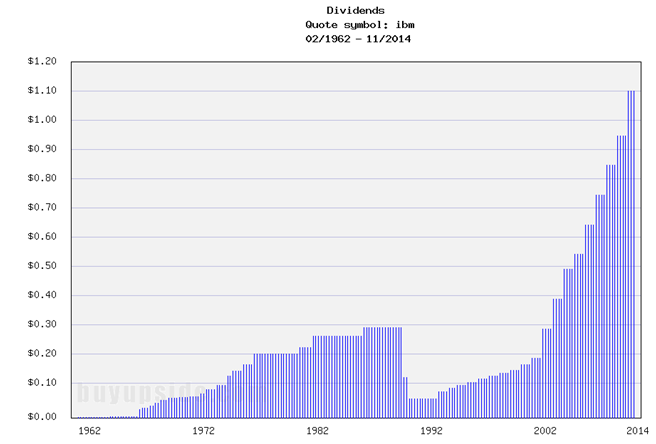

First and foremost, IBM is returning cash to shareholders at a rapid rate. In 2014, IBM paid shareholders $4.40 per share in dividends, which is $4.36B in cash. Besides this, IBM's dividend payments have also been increasing for 19 straight years as shown in the chart below, fully reflecting the company's dedication to such a form of shareholder remuneration

(click to enlarge)

Besides just dividends, the company is also actively repurchasing shares. In fact, the company has bought back $13.5B in shares over the past 9 months, effectively reducing the number of IBM shares outstanding by almost 8% in less than a year. In October this year, IBM authorised $5B more in stock repurchases, in addition to its $1.4B remaining in the same buyback program from the last authorisation. Share repurchases benefit shareholders by allowing shareholders to increase their stake in a company without increasing their share count.

IBM, as a giant technology company with economies of scale, has the ability to take advantage of growth in emerging markets, such as the Middle East and Africa.

A rising middle class and urbanization in these less-developed areas has been driving growth and consumerism, which has resulted in the growth of many companies, including supermarkets, banks and telecoms. These companies, based in less-developed countries, lack the necessary resources and personnel to independently analyze and manage their data, and to create mobile platforms for their customers. Hence, many of these companies will have to outsource some of these jobs to other companies that specialize in this area.

This is where IBM comes into the picture. Being a credible large company with the expertise and skills to help them create such technology, IBM is poised for further growth in this area as less-developed countries in the Middle East and Africa develop, driving further growth in IBM going forward.

-Resources For Turnaround

Additionally, IBM is a giant technology company, with enough financial and human resources to develop new ideas for future growth, and to invest in Research & Development (R&D). I believe that such a quality will allow IBM to eventually shed itself of its non-profitable segments, and to take advantage of new ideas and partnerships for further growth in the future. Although IBM has not fully turned around, there are already a number bright spots within the many operating segments that IBM owns, as shown below.

-Fantastic Opportunities for Growth in IBM's Software Segment

Although IBM's hardware segment is languishing, there are other segments within the company's software segment that are flourishing. For instance, IBM's Big data and business analytics segment grew 8% in Q3 2014, and is expected to generate $20B in revenues in 2015. Additionally, mobile revenues have already doubled year-to-date, and revenues for its security segment are up 20% year-to-date. The company's cloud segment also grew rapidly, with revenues increasing 50% year-to-date.

I want to focus on one of these fast growing segments- the cloud services segment. Although it generated a sizeable $4.4B in 2013, there are no signs of growth slowing down, with IBM quadrupling its cloud data facilities worldwide to 49 in the past 18 months, and striking a partnership with data center provider Equinix (EQIX) for 9 more cloud data centers across the world. The company also stated in this article that 2014 has been "a breakthrough year" for the segment.

There are three main reasons why I am confident that IBM will maintain such incredible growth rates in this area- Growth in the cloud sector, IBM's leading technology and strategic partnerships.

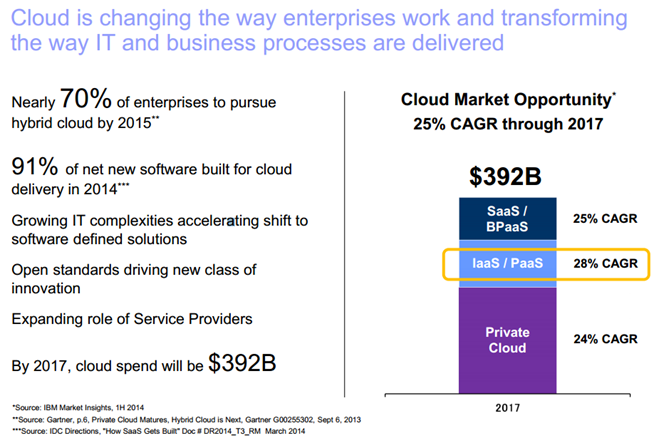

One, growth in the cloud sector. The cloud sector is indeed poised for much growth going forward, with estimates from Gartner indicating that 70% of enterprises will pursue hybrid cloud (a cloud computing environment where an organization provides and manages some resources in-house, and has others provided externally) due to growing IT complexities by 2015. IBM has also estimated that cloud spending will reach a whooping $392B by 2017, which represents a CAGR of 25%. The image below shows more factors contributing towards the growth of the cloud sector.

(click to enlarge)

Courtesy of IBM's 17 September 2014 PaaS Webcast

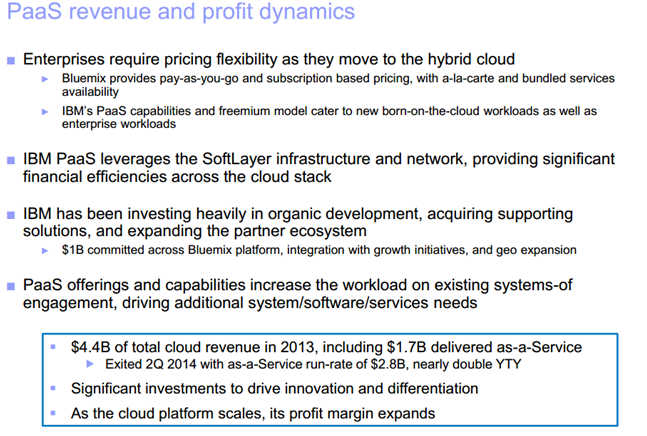

Two, IBM's leading technology. IBM's Bluemix (Platform-as-a-Service) focuses on automation and on runtimes, code and data- all to help the developer start developing web and mobile applications immediately without time lost to setup infrastructure. Enterprise customers are therefore more likely to use PaaS, as it allows a smoother integration of existing systems and applications into the cloud, and to develop and bring their apps to the market more rapidly and efficiently. This saves them a considerable amount of time and trouble. IBM then allows them to use its Bluemix cloud data services to manage the data generated by these apps, and analyze great amounts of data (in many forms).

As shown in the investor webcast slide below, IBM provides customers with a lot of flexibility regarding payment, and has committed to improve the Bluemix technology, with $1B devoted wholly to the platform. It also gives itself a chance to leverage some of their other infrastructure, allowing the company maximum benefit.

(click to enlarge)

Courtesy of IBM's 17 September 2014 PaaS webcast

Since Bluemix has been introduced earlier this year, it has been popular among developers and its target audience, with articles such as this andthis surfacing. In fact, the LinkedIn article (second link) is an article that compared IBM's Bluemix, Microsoft's Azure and Amazon's AWS. The best platform overall was concluded to be Bluemix.

Besides all these information about Bluemix, the third (and probably the best) part about Bluemix and its opportunity for growth is IBM's collaboration with Apple (AAPL)'s iOS system. Initiated in July 2014, I think that this is a win-win situation for both parties. The plan involves IBM developing over 100 industry-specific enterprise solutions in Apple's app store. This, along with the development of IBM cloud services optimized for iOS, targets markets including security, mobile device management and analytics. With Apple being the largest mobile company in the world, this move will allow IBM to reach out to a larger number of developers and enterprises. I believe that IBM's good reputation among the community of developers and enterprises will only improve growth rates in this sector.

Frank Gens from the International Data Corp (IDC) probably put it best, saying:

"IBM's key differentiator and long term strategic bet is its Bluemix PaaS, which they are combining with their analytics capability in the cloud and with Apple's broad reach of mobile devices."

Hence, with such a three-pronged driving force for further growth in this large segment in IBM going forward, I am confident that IBM's prospects will improve going forward, despite being in a turnaround phase.

-The Many Strategic Deals Made Are Assurance of IBM's Credibility

IBM has also reported a string of strategic deals with other companies over the past 1 month, including a 7-year partnership with WPP(WPPGY), the world's largest advertisements company, to enhance and manage the latter's technology platform; a 10-year multi-billion service deal with ABN Amro, a Dutch banking giant to implement a private IBM cloud and to manage services such as servers, storage and application support; Department of Energy contracts worth $325M for IBM to create 2 GPU-accelerated, fastest-in-the-world supercomputers (installation expected in 2017); and a $1.25B outsourcing deal with Lufthansa(DLAKY), where IBM will take over the airline's IT services segment.

All these deals, announced between early November and mid December 2014, are mega-sized, with almost all the deals listed above worth at least $1B. Hence, such a trend fully demonstrates the confidence and faith these large enterprises have in IBM's expertise and the quality of its service. Hence, this shows that while IBM is faltering financially of late due to troubles as stated above, it still remains credible and reliable in the eyes of its many customers.

-Watson's Growth Potential

For those who do not know about Watson, it is IBM's proprietary cognitive technology system that is able to process information more like a human than a computer. As shown in the Watson website, the system has many benefits over normal computers.

IBM also has great hopes for the Watson supercomputer, which is expected to generate $1B by 2018 and $10B by 2024. While these numbers could be slightly exaggerated, I am confident that this technology will be used in many companies and industries in the future, and that it will be a source of growth for the company in the future.

In fact, Watson is already showing potential in the travel, healthcare and food industries. Travel company WayBlazer is already using Watson to help websites create travel plans that fit the interests and budgets of individual consumers. In the healthcare industry, doctors are working with Watson to quickly and safely derive diagnoses and the best treatment plans from the latter's vast knowledge. In the food industry, chefs have also used Watson to enhance their own skills and to create new recipes.

-Shares Proven Cheap on a Conservative Valuation

I will be using the conventional DCF valuation method to value Wisconsin Energy.

First and foremost, I will be calculating the discount rate (weighted average cost of capital) for both the current time period and the terminal time period (10 years later). I will be using the WACC formula in the image below.

Courtesy of Investopedia.com

With the risk-free rate (10 Year Treasury Bonds) at 2.07%, the Equity Risk Premium taken to be 6%, and IBM's beta at 0.63, the company has a cost of equity of 5.85%

Since IBM's interest expense this year of $1.05B has been generated from $33.26B in debt, we get a cost of debt of 3.16%. After a tax rate of 20%, the company's cost of debt is 2.53%.

The company had $39.72B in debt and $22.79B in equity as of fiscal year 2013. Weighting the cost of debt and the cost of equity by these two figures, we generate an initial WACC of 3.74%.

Following this, we calculate the final (terminal) WACC for IBM. For the cost of equity, we will assume that the risk-free rate in the USA stays at 2.07%, the equity risk premium stays at 6%, and the that the company's beta remains constant at 0.63. This yields a cost of equity of 5.85% once again.

For the cost of debt, we will assume that IBM has a debt/equity ratio of 6.09%, the average for the IT industry. In addition, we will also assume that the company's cost of debt decreases from its current 3.16% to 3.07%, which is 1% above the risk-free rate.

Applying the same formula, we generate a final WACC of 5.66%, slightly lower than the initial WACC.

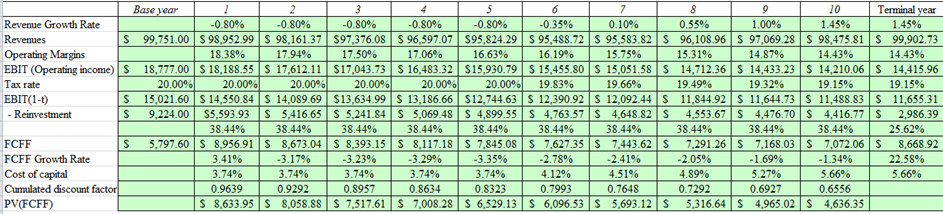

Now, we will estimate the revenue, EBIT and FCF growth IBM will generate over the next 10 years. Here are some assumptions I made during the valuation process:

Revenue Growth Forecast: I will be conservative in this case, and take IBM's revenue growth over the next 5 years to be equal to the growth over the past 5 years, which stands at -0.80%. This growth rate will then increase at a constant rate to 1.45% in the terminal year. Since a rule of thumb in valuation is for the risk free rate to be equal or more than the stable growth rate, I will put the stable growth rate of IBM at 70% of the risk free rate of 2.07%. Such a trend also reflects my general expectations of IBM over the next few years- struggling to turn around for a few more years before finally turning around and experiencing growth. Of course, as stated above, the figures I've used are conservative.

Operating Margins: Operating Margins are expected to converge towards the industry average operating margins of 14.43%. This reflects my expectation that IBM will eventually run out of ways to cut costs (increase margins) further, and will, by then, rely on growth of its other, stronger segments.

Tax Rate: The effective tax rate for Wisconsin Energy is at 20% this year, even though the average effective tax rate for the IT industry is 19.15%. Hence I assumed that the company's tax rate would stay at 20% between year 1 and 5, before declining from 20% to 19.15% at a constant rate between Year 6 and the terminal year.

Reinvestment (Initial Years): Reinvestment refers to the amount the company will spend to grow itself in one fiscal year. It is the sum of Capital Expenditures and the change in Non-Cash Working Capital. I would normally use the sales-capital ratio. But since sales growth is going to be negative for a few years, using the sales-capital ratio would only generate an unrealistic fair value of IBM. Hence, I assumed that the average reinvestment rate (reinvestment/after tax EBIT) over the past 5 years of 38.44% would be the reinvestment rate for IBM over the next 10 years.

Reinvestment (Terminal Year): The reinvestment rate in the terminal year will be computed by taking the terminal growth rate, divided by the final WACC calculated earlier in the valuation, which yields a terminal reinvestment rate of 25.62%

With the above assumptions, we get the following numbers:

(click to enlarge)

All values in Millions

By adding the Present Discounted Value of the FCFF values over the next 10 years, we get a value of $64.456B. The terminal value will be calculated by the formula below, and will then be discounted to give a present value of $135.117B.

By adding the two present values up (PV of Terminal value at $135.117B and PV of FCF values of $64.456B), we get a total present value of $199.572B. Adding the company's current cash holding and subtracting off its current debt holding, the final value of equity is $170.924B. Dividing by its current 989.65M shares outstanding, wits per-share value is $172.71. This is a 14% premium to the last closing price is $151.93.

The valuation proves that not much needs to go right at IBM for valuations to be justified. According to the table shown above, IBM's current valuations are effectively calling for declines of revenues of nearly 3%, along with diminishing margins over the next 5 years (before resuming its growth trajectory to a conservative terminal growth rate of 1.45%). Hence, I believe that IBM is undervalued at today's depressed prices, which give investors a good chance to grab a stake in the Big Blue.

Conclusion

In conclusion, it is undeniable that IBM faces near term challenges and is experiencing languid revenue growth at the moment- typical of a company that is in the process of turning around. Although this is the case, the Big Blue definitely has the financial and human resources to turn around strongly, and is poised for further growth into the future after this turnaround phase. Besides reasons that suggest we could see significant growth going forward, IBM is also undervalued according to a conservative DCF valuation model, with potential upside of 14%. Furthermore, with the company returning nearly $18B in the first 9 months of this year as dividends and share buybacks, it definitely makes sense for long-term investors (and dividend investors) to take advantage of the low prices at IBM to start building a position in this world-class technology leader. After all, as Bernard Baruch once said, "Buy your straw hats in the winter."

Monday, 3 December 2012

Friday, 9 November 2012

New Articles

Tuesday, 6 November 2012

Some Articles On Seeking Alpha

Hi all,

I have been working on these articles (and published them) over the past week [Seeking Alpha], please click on the links provided to read the articles:

I have been working on these articles (and published them) over the past week [Seeking Alpha], please click on the links provided to read the articles:

1. 8 Consumer Stocks With 40 Years Or More Of Consecutive Dividend Increases

Happy Trading!

Kang Wei

Friday, 26 October 2012

2 New Articles On Seeking Alpha

Tuesday, 23 October 2012

Article No.4

Hi all,

Got a new article, on Seeking Alpha again. Follow this link to read the article.

Happy Trading

Kang Wei

Subscribe to:

Comments (Atom)